The Short Version

- Recent ICSC research points to a consumer who remains active and store-oriented, even as higher prices and household budget constraints influence spending decisions.

- Physical retail continues to play a central role in shopping behavior: 82% of consumers recently spent money in-store, compared with 71% online.

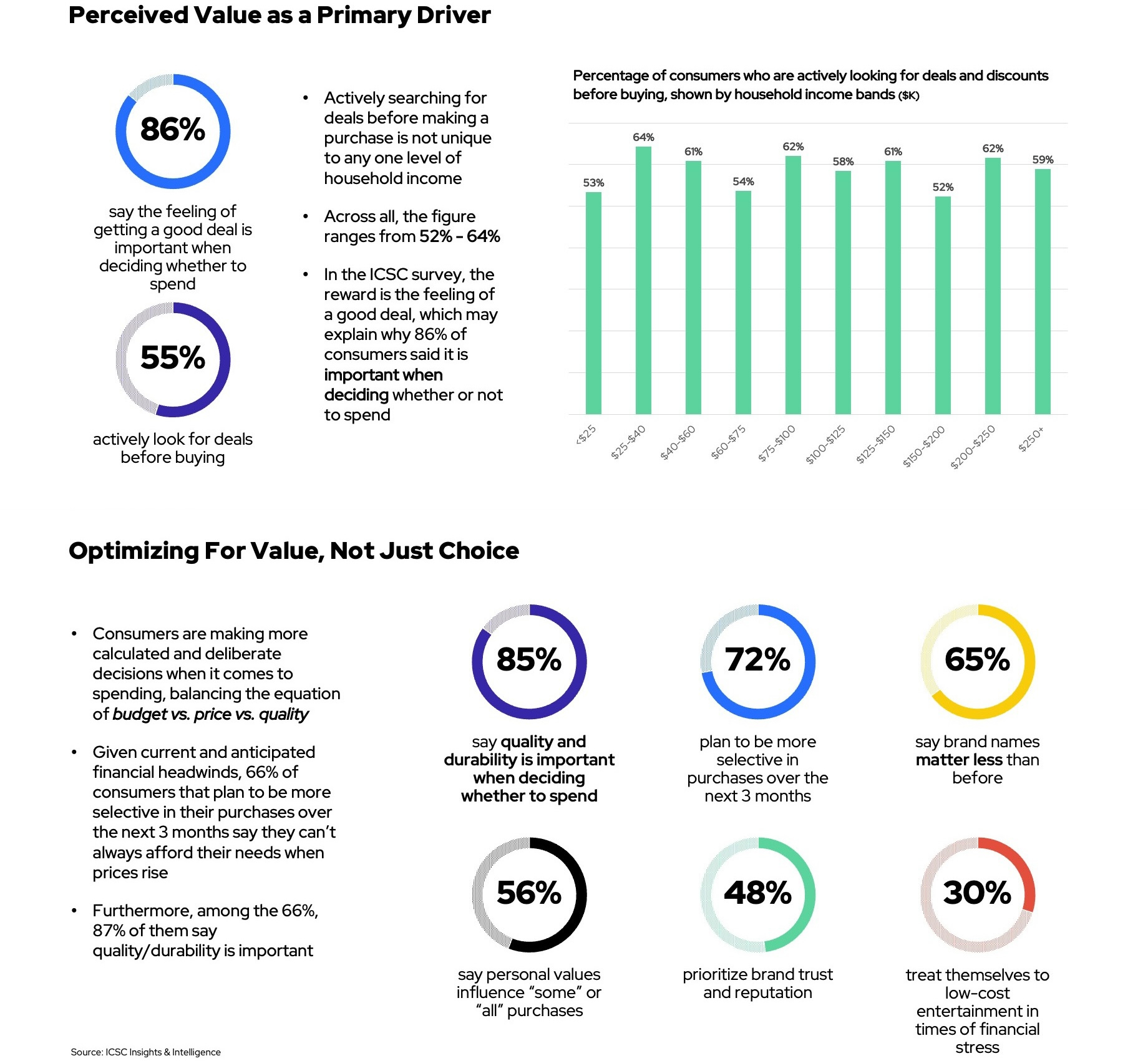

- Consumers are becoming more selective and value-driven, with 86% saying getting a good deal is important when deciding whether to spend.

- Spending patterns vary by income, age and category, but the broader takeaway is that consumers are still engaged and willing to spend when the product’s value proposition is clear.

Consumers Remain Active as Higher Prices Reshape Spending

Recent ICSC Insights & Intelligence consumer surveys point to a shopper who is still active, still store-oriented and increasingly focused on value. Physical retail continues to play a central role in how consumers browse, buy and fulfill purchases, even as higher prices, essential expenses and household budget considerations influence how they spend. The result is a landscape that remains active but increasingly selective and value-driven.

The just over 2,000 total U.S. respondents were split evenly across a late February survey and an early April survey.

Consumers continue to engage in in-store shopping and allocate spend toward discretionary categories while exhibiting increased deliberation and selectivity in purchase decisions. Overall, 76% of U.S. consumers say their monthly spending has increased this year, though 72% of those cite rising prices as the reason for increases in spend. It also shows though that consumers continue to shop even as prices have increased.

Physical Retail Remains Central to Shopping Behavior

Even as consumers become more selective with their spending, physical stores remain central to how consumers shop. The survey suggests 82% of consumers recently spent money in-store, compared with 71% who spent online. Consumers also visited stores 6.4 times per month on average, showing that in-person shopping continues to be a core part of their routine.

Neighborhood and community centers were especially popular, as 65% of consumers had visited one recently. Nearly half of consumers, 49%, visited an enclosed mall. The survey also shows that omnichannel habits support rather than replace in-person shopping: Among the 36% of consumers who used click-and-collect, 70% visited neighborhood or community centers and 60% visited malls.

The findings indicated that stores continue to play a central role in the shopping journey. Even as consumers become more selective in their spending, they continue to turn to physical retail for convenience, immediate access to products, browsing and fulfillment of everyday needs.

Higher Prices Are Shaping Spending Patterns

Higher spending does not necessarily mean consumers feel free to spend without limits, however. While many consumers remain able to absorb higher costs and maintain their spending levels, higher prices and new expenses are putting increased pressure on household budgets, prompting some consumers to adjust what they buy. Among those who say their monthly spending has decreased, 46% are reducing nonessential purchases, while 39% cite concerns about the economy or inflation.

The distinction is important: Consumers are still active, but as everyday costs rise, many are making more careful decisions by prioritizing purchases, comparing options and making more deliberate choices.

Essentials Are Consuming a Larger Share Within Household Budgets

Essential expenses take up a large share of consumers’ budgets, leaving less room for flexibility. Consumers estimate that 70% of their budgets go toward essentials, while the remaining 30% goes toward nonessential purchases. That balance helps explain why consumers are being more selective with discretionary purchases as they manage higher costs.

Those budget dynamics show up in other areas of the ICSC Insights & Intelligence consumer data, as well: 59% of consumers cannot always buy necessities when prices rise, and 64% say the economic outlook affects their current spending. Importantly, 38% of consumers are taking a pragmatic approach to an increase in costs by managing their budgets thoughtfully and decreasing nonessential spend over the next three months.

Value Is Shaping Purchasing Decisions Across Income Groups

Shoppers are not simply choosing the lowest-price option. Instead, the data suggests, they think more carefully about what makes a purchase worth it. Price matters, and so does quality, durability, brand trust and the emotional satisfaction of getting a good deal.

That value-focused mindset appears across all income groups. Overall, 55% of consumers say they actively look for deals before buying, while 86% say getting a good deal is important when deciding whether to spend. Deal-seeking is not limited to lower-income households, either; the share of consumers looking for deals ranges from 52% to 64% across income groups.

Consumers also are weighing long-term value, as 85% say quality and durability are important and 72% plan to be more selective in their purchases over the next three months. At the same time, 65% say brand names matter less than they used to, though 48% still prioritize brand trust and reputation. More than half, 56%, say their personal values influence some or all of their purchases, pointing to a more intentional approach to spending.

Discretionary Spending Is Becoming More Selective

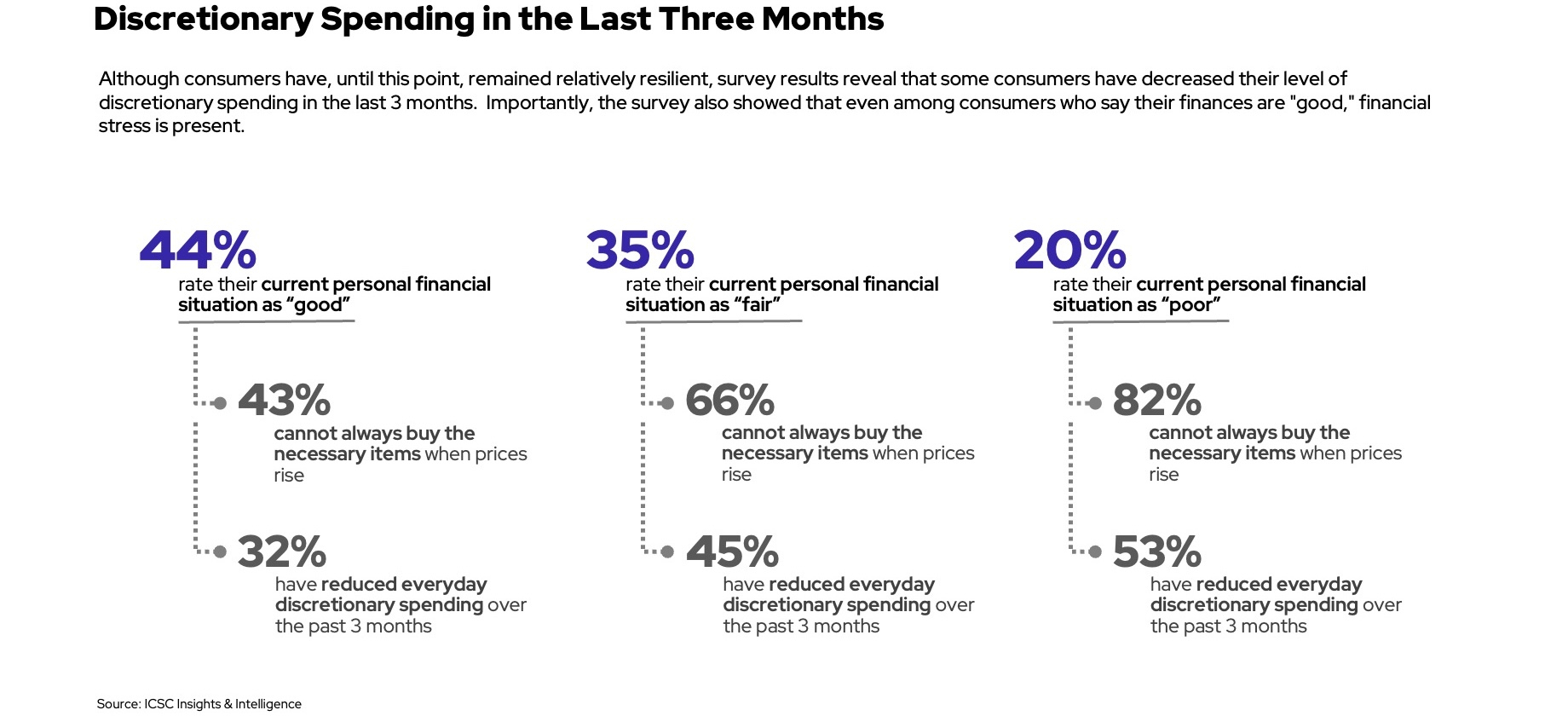

Consumers are protecting their everyday and essential-adjacent spending while taking a closer look at higher-ticket or optional categories. Even among those respondents who characterize their finances as “good,” 32% have reduced their discretionary spending over the past three months. That number rises to 45% and 53% for those who rate their finances as “fair” or “poor,” respectively.

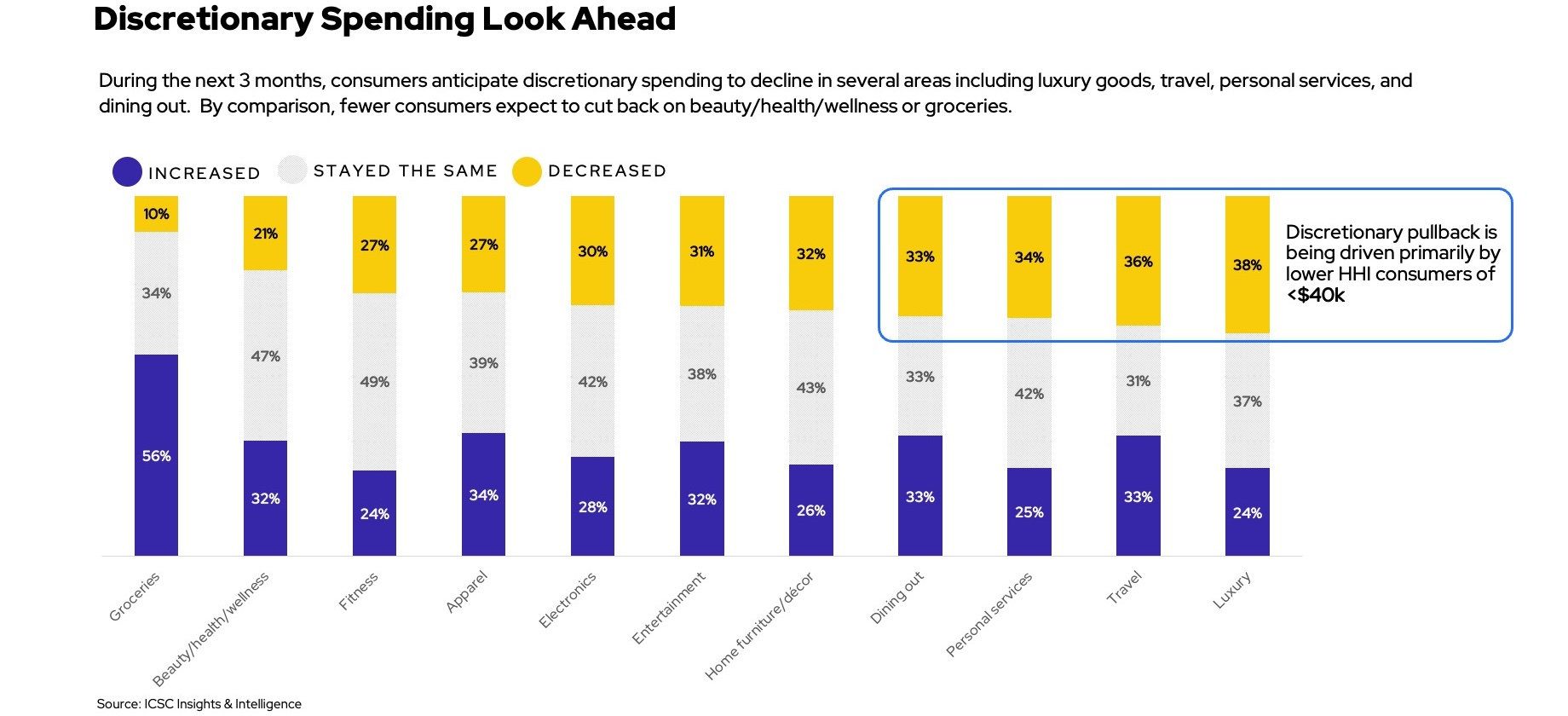

Looking ahead to the next three months, respondents anticipated mostly maintaining their levels of spending in categories like groceries, wellness/beauty/fitness and apparel, while pulling back more in other categories, including travel and dining out. Notably, expected decreases in discretionary spending concentrate more among households earning less than $40,000 per year.

Consumer Spending Patterns Vary by Income and Age

The survey also shows that consumer sentiment and spending behavior vary widely by income and age. Some consumers are still spending freely or selectively trading up, while others are watching their budgets more closely, looking for deals or cutting back on nonessential purchases.

Income plays a clear role in how consumers view their financial situations. The data identifies $75,000 in household income as an important inflection point in financial sentiment, and the divide becomes even more pronounced at $150,000. This pattern suggests that while higher income improves financial confidence, it does not fully insulate consumers from the effects of rising costs. Still, the effects of higher prices are not limited to lower-income households. Even among consumers who describe their finances as “good,” 43% cannot always buy necessities when prices rise. Among those who describe their finances as “fair,” that share increases to 66%, and it rises further to 82% among those who describe their finances as “poor.”

Income plays a clear role in how consumers view their financial situations. The data identifies $75,000 in household income as an important inflection point in financial sentiment, and the divide becomes even more pronounced at $150,000.

Younger consumers are more likely to have increased their nonessential spending, while older consumers are more likely to have pulled back. Among consumers 65 and older, 27% are trading down to cheaper alternatives and 20% are skipping purchases altogether. By comparison, only 3% of older consumers are splurging or choosing premium options, suggesting a cautious approach among older shoppers.

Consumers Remain Engaged as Value Becomes More Important

ICSC’s survey points to a consumer who remains engaged with stores, responsive to convenience and willing to spend when the value proposition is clear. At the same time, many consumers are budgeting carefully, comparing options and making more intentional decisions about discretionary purchases. The takeaway is not that consumers have stopped spending but rather that consumer spending is becoming more selective, more value-driven and more varied across income levels, age groups and categories.

By Katie Kervin

Managing Editor, Commerce + Communities Today