Over the past year, a host of bad things — new risk-retention rules and a wall of bond maturities among them — were supposed to punish the commercial-mortgage-backed-securities market. But the worst didn’t happen.

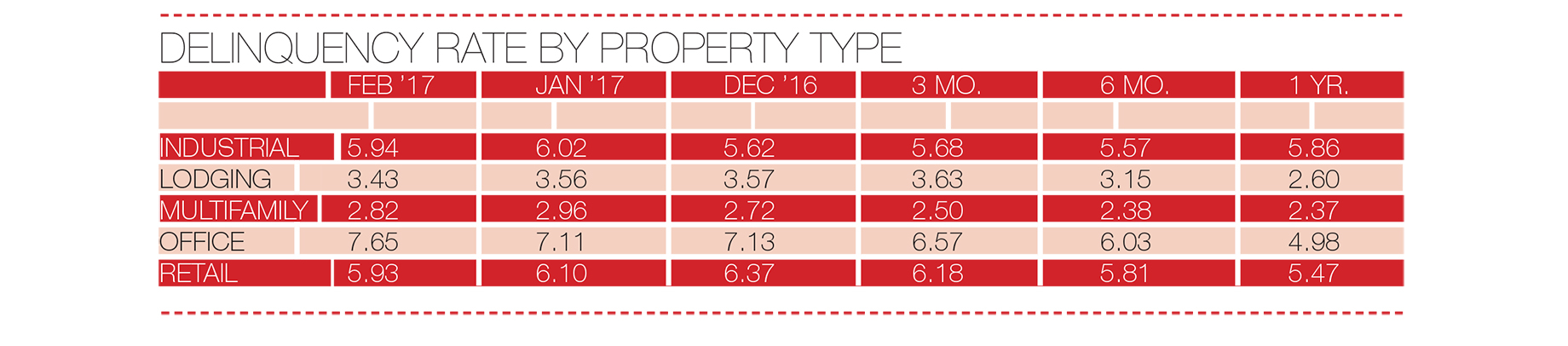

The Trepp CMBS Delinquency Rate has been moving steadily higher during the past 12 months. According to the firm, the delinquency rate for U.S. commercial real estate loans in CMBS was 5.31 percent, a month-on-month increase of 13 basis points in February. Retail underperformed the broader market, with the retail CMBS segment posting a 17-basis point decline in the supply of delinquent loans to 5.93 percent.

The most recent problem to emerge is the announcement that J.C. Penney Co. plans to close 140 stores, news that followed hard upon Macy’s department store closings and retailer bankruptcy filings. “The planned closures will weigh on some loans within some Fitch-rated CMBS pools,” according to a Fitch Ratings analysis. JCPenney was listed as a top five tenant in 136 properties within 122 CMBS transactions, the credit ratings agency says. “The potential closure of these stores will have a direct effect on the respective loans regardless of whether the store itself is collateral for the loan,” reported Fitch. “This is due to declining rental income, reduced foot traffic and/or potential co-tenancy lease clauses affecting the overall property.”

Some owner-operators view a Penney closing as an opportunity to re-lease the space for other purposes or to a group of stores, notes Huxley Somerville, a Fitch managing director in New York City. “If the mall operator doesn’t have the capital or imagination to convert the space, or the mall is unlikely to attract new tenants, the property could potentially be valued at less than it was originally.”

Last year CMBS volume was about $70 billion, reports Manus Clancy, a senior managing director at New York City–based Trepp. “The market was supposed to do about $100 million, but spreads widened in the second quarter, and that put a chill on things,” said Clancy. “That was followed by a lot of volume as issuers were trying to get deals done before risk retention kicked in.”

The new risk-retention rules meant that issuers had to retain 5 percent of the bonds being sold, and they had to hold them for the life of the deal, observers say. “There was this huge fear — which reminded me of Y2K fear, in that this was going to be a disaster — that no one wanted to keep a piece of the bond on the books, and pricing was going to jump 100 basis points,” recalled Dan Gorczycki, a senior director at New York City–based Avison Young. “Like Y2K, it turned out to be much ado about nothing. Deal costs may have increased by 5 basis points.” The only effect Gorczycki could see was that it made the big lenders more competitive while pushing out the lesser issuers that could not absorb even the small extra cost.

This year the CMBS market got off to a slow start, in part because there was a lot of issuance at the end of last year, when everyone wanted to get the bonds off their balance sheets before risk retention kicked in, says Somerville. “We started 2017 with not a lot of dry powder.”

“This year the CMBS market got off to a slow start, in part because there was a lot of issuance at the end of last year”

That wall of maturing loans ended up being a mere hurdle, because when interest rates started going down, any reduction in value or net operating income was offset by lower interest costs, says Gorczycki. “If you were refinancing a 7 percent loan and now got a 4.5 percent loan, that made up for the ills of being overleveraged,” Gorczycki said. “Your interest costs went down, so you were OK.” What eventually happened was the better loans were able to get refinanced, not the poorer performers.

“We have seen delinquency rates jump by about a full percentage point over the last year, from about 4.15 percent to 5.15 percent, and that is a reflection of loans coming due that can’t find refinancing,” said Clancy. “With low interest rates for the last several years, a lot of high-quality loans were refinanced. That also helped middling properties get through. This stuff went away, and what you were left with was the weaker-credit stuff, and that’s what’s pushing that delinquency rate higher. All eyes are on retail right now. People are lining up their bets on either side of the table.”

Clancy points to CMBX — a synthetic tradable index that references a basket of 25 commercial-mortgage-backed securities. The index is administered by a company called Markit, which issues a series every year. “The issues everyone watches are CMBX6 and CMBX7, which are heavily skewed toward retail,” Clancy said. “Those that feel the department store story is overblown are going long on CMBX, and others who feel department stores are dinosaurs say this is going to be the next ‘big short.’”

For nontraders, Gorczycki offers a simpler view: “If you are a grocery-anchored shopping center or you are a Simon mall, CMBS loves you,” he said. “CMBS still loves retail — but only the best retail.”

By Steve Bergsman

Contributor, Shopping Centers Today